Apply For A Loan Today

Tell us some basic details about your project below and let us work on structuring the best loan for you. We value your time and will reach back out to you shortly!

Hard money loans in Texas

Real estate, like any investment strategy, requires math. Whether you’re flipping houses, investing in wholesale, building, or getting a real estate license—you need some basic math skills.

If math is not your forte, though don’t worry. There’s a handful of formulas to get familiar with, but nothing you can’t handle. Sharpen those #2 pencils and let’s go.

You don’t need to sign up for math classes at your local community college (although a pre-algebra class wouldn’t hurt if you’re especially rusty), but you will want to take the time to learn the basics. Math won’t be the majority of your daily work, but you don’t want to let it hold you back either.

The good news is that the math you will need for real estate investing and/or selling is not that difficult. If you’ve been adulting for any period of time, you’re probably already familiar with the basic concepts and processes: multiplication and division, percentages and simple ratios, concepts like interest rates, etc.

Real estate math is just about applying those principles in new ways, using a handful of new ratios and formulas that are not that difficult to get used to.

Before we talk about those formulas, there are a few terms to make sure you’re familiar with:

Real estate math is based on some very simple formulas. This list might seem daunting at first, but don’t be discouraged.

First, you won’t use all of these formulas. Some are used most often by real estate agents. Others are used more by investors.

Second, once you’ve applied these formulas a few times—in class, on exams, or just in real life situations—they will start to become second nature. Start by memorizing the ones that are most relevant to you, but remember that they will get easier the more you use them.

The simple interest formula helps you calculate the final amount of a loan, based on the principle and interest rate.

The variables are defined as:

Remember that to convert percentages to decimals you simply move the decimal point two places to the left. For example, 50% = 0.5

Time is always expressed in years, so if you’re considering a time period of six months, for example, your t value would be ½ or 0.5.

So if the principal amount of the loan is $200,000, at a 10% interest rate, for six months, the simple interest formula becomes A = 200,000(1 + 0.10 * 0.5). Here, A = $210,000.

Sometimes confused with the “simple interest formula,” the interest formula allows you to calculate the interest rate.

Many of the variables here are the same:

Using the same scenario, the amount paid in interest on this loan is expressed as I = (200,000)(0.10)(0.5), or I = $10,000.

The gross rent multiplier helps investors determine the rough value of a rental property—before subtracting expenses like taxes, maintenance, etc.—to get a quick idea of how fast the property will pay for itself.

If an investor, for example, is thinking about purchasing a duplex for $500,000 and total rent for each home is $3,000/mo ($36,000 per year), the GRM formula looks like: GRM = 500,000 ÷ 36,000, so GRM = 13.9

The GRM is expressed in months, so this property would pay for itself in about 14 months. Remember, though, that this does not include other fees, so it’s not completely accurate. The GRM is a starting point for investment considerations.

Calculating property tax requires a short series of simple formulas. The property tax formula is:

First, to find the assessed value, multiply the property value by a local assessment percentage, so:

You can find the assessment percentage from public records, either online or by calling your county.

So if that duplex is valued at $500,000 and the local assessment percentage is 10%, your assessed value = 500,000 x 0.10, or $50,000.

The mill levy number is available from a local assessor. If they give you a whole number it needs to be divided by 1000 for the proper ratio. If the local mill levy rate is 90, it would be 0.090 for your equation. That means the property tax = $50,000 x 0.090, or $4,500.

The Mortgage Rule of Thumb is a good real estate math formula for agents to have in their back pockets, for their clients. It states that a mortgage should be no more than 28% of pre-tax income and no more than 36% of someone’s total debt.

and/or

The LTV is a ratio formula that lenders use to evaluate our level of risk, but it’s one that real estate investors need to understand as well.

If a buyer needs a $130,000 loan for the purchase of a $150,000 home, for example, the loan to value ratio = 130,000 ÷ 150,000, which comes to 0.867 or 86.7%.

The LTV is used by lenders to determine interest rates: the greater the risk, the higher the interest rate.

Hard money lenders will sometimes determine the LTV using the property’s after-repair value (ARV). If an investor asks for a $400,000 loan to purchase a distressed property that they plan to flip for $500,000, the LTV might be expressed as LTV = 400,000 ÷ 500,000.

The discount point formula helps a long-term buyer understand if discount points are a good investment.

Let’s imagine that a homeowner is considering a 30-year, $200,00 mortgage with a 3% interest rate. At 1% of the principal, each discount point would cost $2,000 and probably lower the interest rate by 0.25%. If the borrower decides to purchase two discount points at closing, they will spend an additional $4,000 and reduce the interest rate by 0.5% (from 3% to 2.5%).

The commission formula is a simple percentage calculation to determine how much an agent or other professional’s commission will be on a sale.

If you’re working with a real estate agent who has a 6% commission rate, for example, and together you sell a flip for $250,000, calculating the dollar amount of your agent’s commission would look like: commission = 250,000 × 0.06, or $15,000.

The 70% rule is a guideline in real estate investment that states a buyer should not invest in a property for more than 70% of its after-repair value (ARV). The 70% rule is another simple percentage calculation that looks like this:

Imagine a flipper is considering a distressed property for $375,000, with an ARV OF $500,000. Because 500,000 × 0.70 = 350,000, that investor should negotiate for a sale price of $350,000 or pass on that opportunity.

The cash on cash return is generally a method of evaluating an investment in rental properties. It compares cash invested to cash generated by cash flow generated:

If an investor contributes a $50,000 down payment on a rental property that generates $36,000 per year, then, the cash on cash return = 36,000 ÷ 50,000, or 72%.

There’s no right or wrong cash on cash return value, but most investors will develop their own limits.

The debt service coverage ratio is used in rental and commercial property, to help investors and lenders evaluate the borrower’s capacity to repay the loan, based on the property’s cash flow.

The debt is sometimes a calculation of its own, including the principle, interest, taxes, insurance, and any required association fees.

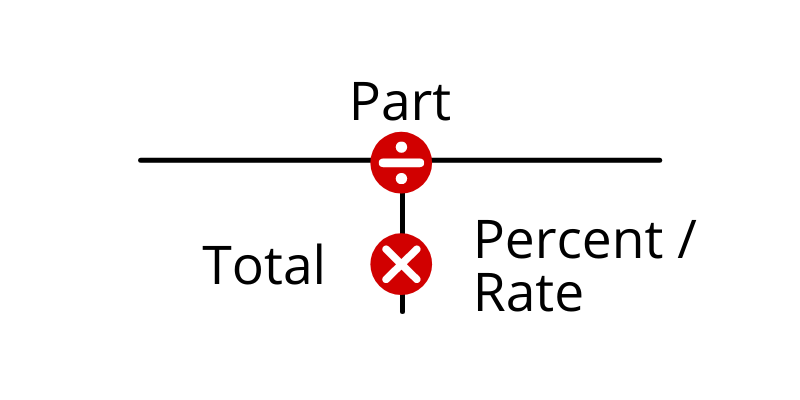

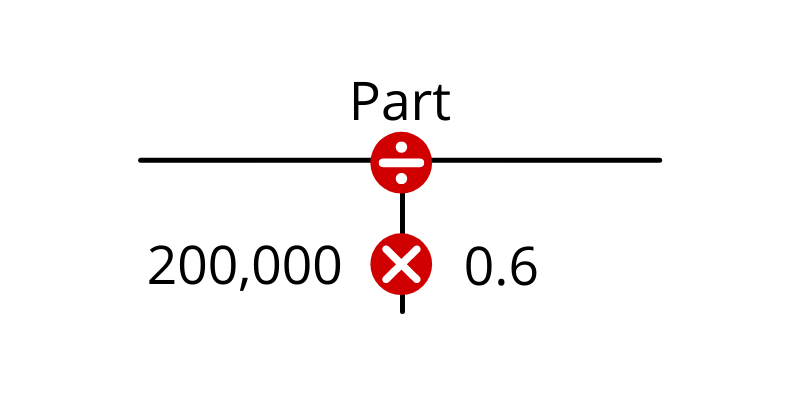

The T-bar method is a strategy for simplifying the use of percent calculations. Most simple percent calculations use the same basic formula and rules, but it can be difficult to remember which values go where in the equation.

The T-bar method places three common values: part, whole, and percent around a T-shaped frame:

For any percent equation, then, you can plug in the two values you have, and use the function between them (division or multiplication) in order to calculate the one you are missing.

If you need to calculate a commission amount, for example, you can plug in the sale of the property and the percent of the commission (as a decimal point), to figure out how to calculate the amount:

Thus, the commission (the part) = the whole sale price × the commission percent, or Commission = 200,000 × 0.60.

Proration commonly comes into play in real estate investment, when a seller has already prepaid annual taxes on a property that they sell mid-year.

Let’s assume that a homeowner prepaid $6,600 for property taxes, for example. They then sell the property in August, so the buyer needs to reimburse the seller for the last four months (September through December) of prepaid property taxes.

There are countless situations when proration may need to be considered, so there isn’t one standard formula. In this case, we would divide the prepaid, annual amount by 12 months (6,600 ÷ 12), to get a monthly value of $550. We would then multiply that monthly value by the four remaining months (550 × 4), to get a final value of $2,200 that the buyer owes for prepaid taxes.

You probably didn’t get involved in real estate out of a love for calculations and mathematical equations, but math is (for better or worse) a crucial part of real estate selling, investing, and construction. Fortunately, real estate math is not complicated and you’re probably familiar with some of the basics already.

There is a decent list of equations to get comfortable with, but the more you use them in the wild, the easier it will be. Take every opportunity to practice with them, even when you don’t necessarily have to, and you’ll be a whiz in no time.

Pro tip: If you do struggle with some of the basics, there are free online resources that can help. The Khan Academy, for example, has a great pre-algebra course that can get you up to speed.

Tell us some basic details about your project below and let us work on structuring the best loan for you. We value your time and will reach back out to you shortly!